TerraVest Industries

The effects of a good capital allocation in a "mediocre" business

TerraVest Industries, Inc. ($TVK.TO) is not a company that stands out as having a huge competitive advantage or an interesting business model. The most attractive thing about TerraVest is that the management team (which owns a large portion of the company) is able to reinvest the cash flows generated to acquire new profitable businesses at low prices and buy back shares, increasing earnings and Free Cash Flow per share. I believe that being such a small company (with a market cap of $424M CAD as of today) and being part of many fragmented industries, TerraVest is likely to be able to continue buying businesses for many years to come (long term reinvestment opportunity with high rates of return).

If we look at TerraVest's chart, the first thing we can appreciate is its huge 85% drop from the 2005 peak to the 2010 bottom, for a subsequent +1,200% recovery until today. This probably leads many investors to think that it is a cyclical company (a portion of its business is cyclical) or that it takes high risks, and that such a huge drop is likely to be repeated in the future. The reality is that TerraVest is nothing like it was in the run-up to 2010.

2010: The activist investment of Clarke Inc.

Terravest has completely different assets and businesses than it did in 2005-2010.

Clarke Inc. which defines itself as "an investment firm with the objective of maximizing shareholder value" built a significant position in TerraVest to influence business decisions and unlock shareholder value. In 2010, TerraVest started to divest its bad businesses (by selling them) with the goal of transforming itself into a Free Cash Flow generating company with a good balance sheet.

In the 2011 annual report, we can see how they explain some of their sales (in 2011, trading at 2 $CAD, TerraVest's market cap was around 40 M $CAD):

On February 4, 2010, sold its interest in the assets and operations of Ezee-On to a subsidiary of Buhler Industries Inc. for $14.5 million.

On March 2, 2010, sold all of the assets of Stylus to certain Stylus Shareholders for $6.5 million.

On December 20, 2010, sold its interest in the assets and operations of Don Park Canada to Rona Inc. The Fund received $22 million at closing.

With the proceeds received from the sale of these assets, they repaid their debt (they repaid 4 million of long-term debt and 16.5 million of short-term debt). In 2012 they repurchased 36% of the outstanding shares through a tender offer and in 2013 they declared a quarterly dividend and restructured all their remaining debt at lower interest rates (due to their improved balance sheet).

Quite an activist investment isn't it? In the years that followed Clarke Inc. continued to increase its positions in TerraVest until it owned 30% of the company which has become a multibagger.

2014: The beginning of inorganic growth

In 2014, with a good balance sheet and generating Free Cash Flow, they started with the second part of the strategy, which they are still implementing, the acquisition strategy.

The key to this strategy is that they are very disciplined with the prices they pay for businesses. In addition, something that surprises me positively is that while they have been acquiring new businesses, they have managed to significantly reduce outstanding shares (from 2017 to 2021, before they did issue shares to finance purchases) and have maintained reasonable Debt/EBITDA ratios. Here is some data taken from TerraVest's annual reports:

The first thing you notice in the table above is that sales have increased tremendously since they started the acquisition strategy. Regarding pre-tax profits, they have also increased a lot. But what happened in 2016 that they fell so much? In their FY 2016 Management's Discussion and Analysis report they comment that one of their most cyclical segments (Fabrication) suffered large declines due to low raw material prices. Nevertheless, the segment continued to be profitable and they took the opportunity to make two acquisitions at very good prices. Another of their cyclical segments (Service) also had a bad year. As I said at the beginning, it is not a perfect business, and it is likely to have bad years again in the future, but the capital allocation strategy is very good and the management is aligned with shareholders.

And what prices do they pay for their acquisitions? We have already seen that they finance acquisitions with cash flows from the business and also with some debt within reasonable levels. Now let's take a look at the prices paid for acquisitions, to do so, I have relied on this presentation by Guy Gottfried (founder of Rational Investment Group).

In the combination of all acquisitions, they have invested 95 million (Guy Gottfried includes expansion capex in the investment cost) and have earned 28 million annual pre-tax FCF, the average multiple paid for acquisitions is 3.4x EV/pre-tax FCF. (Note: There is also a video of Guy Gottfried's presentation). Indeed, very low prices!

In addition to making acquisitions, they invest in the acquired businesses with the following criteria:

Increase the range of products on offer.

Expand production capacity

Increase efficiency

Increase quality

Obtain an attractive return on investment

Management and insiders

In the January 2022 Management Information Circular we can see a lot of information about the company's insiders.

Dustin Haw has been the President and CEO of TerraVest since 2014. Prior to joining TerraVest Industries he served as Vice President of investments at Clarke Inc. He owns 91,466 shares (C$2.1 million) which is 0.5% of the diluted shares outstanding and his annual compensation is $391,106 CAD. There is not much information on the internet about him, and he owns, compared to other insiders, few shares. I understand that he was one of Clarke Inc.'s top employees and was put in charge of TerraVest to control the situation. The other insiders own more shares.

Charles Pellerin is the largest shareholder and owns 3,532,900 shares (CAD$83.7 million) which is 19.7% of the company, and his annual compensation is CAD$150,000. Charles is the Chair of the Board of Directors and is also an insider of Clarke Inc. and sits on its Board.

Dale H. Laniuk owns 11.6% of the company ($49 million) and his annual compensation is $25,000CAD. Dale is a retired investor and was the President and CEO of TerraVest from 2012 to 2015.

Mawer Investment Management Ltd. owns 14.4% of the shares. Mawer is a private investment firm that manages USD 77 billion in assets for individual and institutional investors.

List of investors with more than 10% of the company's shares:

IMPORANT: Clarke Inc. previously owned 32% of TerraVest shares, but Clarke distributed these shares to Clarke Inc. shareholders by way of a dividend where they received one TerraVest share for every 3 Clarke shares. All of this is explained in Clarke’s 2020 annual report and in this presentation. Clarke is an activist investment fund, and they have considered their work to be done at TerraVest, but Clarke insiders still hold a lot of shares and the company is continuing with its acquisition strategy.

Business Model

Normally, investment theses would start with the company's business model, but I wanted to leave that for later, since for me, the most important thing in this company is the capital allocation. Anyway, the business model is extremely important, so let's get to it:

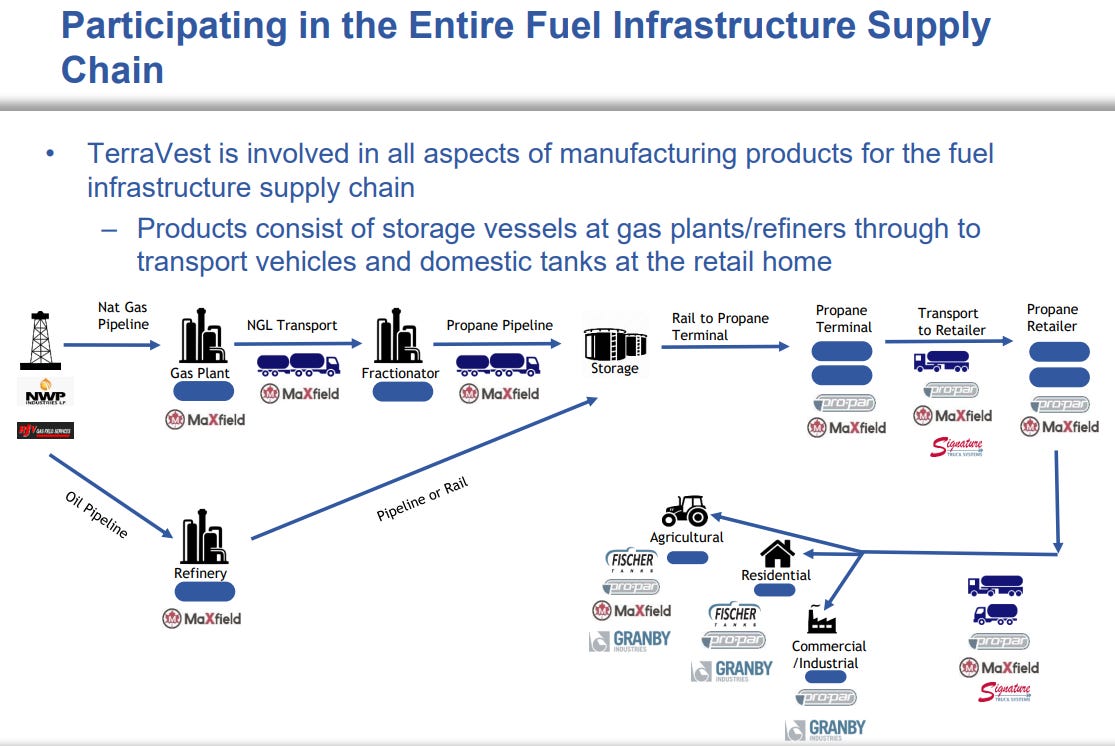

TerraVest is a diversified industrial company that manufactures and sells products and services to various markets including: energy, agriculture, mining and transportation. Its products are sold in Canada (56% sales 2021) and the United States (44% sales 2021). TerraVest is looking to make acquisitions of businesses that complement its operations and allow for synergies after integration.

Some of TerraVest's known customers include:

Home Depot

Shell

Repsol

ExxonMobil

Terravest divides its business into three segments, ordered from largest to smallest::

1-Fuel Containment (60% of sales and 77% of Net Income in 2021)

This segment includes the sale of products related to fuel containment, for example:

Solutions for the transportation and storage of LPG (Liquified Petroleum Gas), propane and anhydrous ammonia.

Fuel storage solutions

Furnaces and boilers

Products are sold through distributor networks and end users are fuel distributors, transportation companies, and industrial, commercial and residential consumers. Competition is high in all product categories and remaining a leader requires national distribution, product innovation, customer service, competitive pricing and access to capital.

Segment risks:

An increase in oil prices (quite likely in my opinion) could reduce demand for storage tanks and furnaces in homes.

Demand for storage tanks in homes could decline due to a decline in home sales (quite likely with rising interest rates). New homeowners are more likely to change the tank.

2-Processing Equipment (35% of sales and 20% of Net Income in 2021)

This segment includes the sale of processing equipment for various markets including: oil and gas, agriculture, transportation and mining. Products are custom designed and manufactured in low volume batches.

Demand for the products in this segment are dependent on the investments of the Oil and Gas industry, making it a more cyclical segment. If energy prices remain high, this segment will likely benefit (as the industry will have more money to invest). If energy prices were to fall, this segment would suffer.

3-Service (5% of sales and 3% of Net Income in 2021)

This segment provides services to oil and natural gas wells. Sales depend on the hours contracted by customers and fluctuate cyclically based on customer needs. Commodity prices, competition and weather can affect this segment. Fortunately, even though it is a highly cyclical segment, it is the smallest of all.

2022: How is the business today?

On August 9, 2022, the board explains that:

"Most of TerraVest's businesses are experiencing increased demand, particularly those with exposure to energy end markets. However, global supply chain disruptions, labor shortages and rapid cost inflation have made it difficult to increase capacity to meet this increased demand. TerraVest will remain vigilant in supporting its operations, managing its cost structure and will make targeted investments in manufacturing efficiency improvements, as well as continuing its acquisition strategy as opportunities arise.”

In the historical data table I have marked that FY2021 sales were 307.5 million. Well, in the first nine months of FY2022 they are already at 414.3 million (an 83% increase in sales over the first nine months of FY2021).

Organic sales growth for these nine months is +20% due to an increase in demand for its products. And the rest? Well, it is of course inorganic growth due to the acquisitions of ECR International, Mississippi Tank and Manufacturing Company (MPC) and 66.8% of Green Energy Services Inc. (GES). In addition, part of the increase in sales is also due to price increases of its products to combat inflation in cost increases in both raw materials and wages.

Despite this strong increase in sales, we can see that profits have risen practically nothing in these 9 months. Why is this?

In the first 9 months of FY2021 TerraVest received 12 million in covid-19 subsidies which inflated profits. In the first 9 months of FY2022 it has received 2.4 million in subsidies (in 2023 it will no longer receive anything). These subsidies are recognized as Net Income.

Cost inflation has partially affected their profit margin, although they have been able to pass on much of these increases to their customers.

TerraVest used debt to acquire 3 companies and finance its working capital so debt financing costs have increased from 2.8 million to 6.3 million in these 9 months.

Regarding the segments, the smallest and most cyclical segment (Services) is in its best moment with the high energy prices multiplying by ~6 times its sales and profits, although this growth is almost all inorganic: Services organic growth is 32%, the rest is due to the acquisition of GES. The Fuel Containment segment has grown by 13% organically and the rest is due to the acquisitions of ECR and MTC. The Processing Equipment segment grew 31% organically and is also positively affected by energy prices, although it is negatively affected by inflation, lack of employees and supply chain issues.

Valuation

Diluted shares outstanding (June 2022): 18,126,554

Share price (October 29, 2022): $23.71CAD

Market Cap (diluted): $429,780,595CAD

Net debt: $253,800,000CAD

Enterprise Value: $683,500,000CAD

The valuation gets a bit complicated as:

MTC was acquired on March 11, 2022 (4 months of the last 9 do not include its results.) Since March 11 it has generated 1.5 million Net Income, but to normalize it, I will add another 1.6 million since 5 months have not been accounted for). For EBITDA I consider it to be 2 million (although it is probably higher).

GES was acquired on November 1, 2021 (1 month out of the last 9 that does not include its results). Anyway, in this case I will not make any adjustment since it is only 1 month.

In addition, for my calculations, I will make the following adjustments:

I'm going to subtract subsidies from 2.4 million.

I'm going to use the filing data for the 9 months ended June 2022 and normalize it as if it were for a full year (multiplying by 12 and dividing by 9 months).

Net Income Normalized = (29,8 - 2,4 + 1,6) x 12/9 = 38,7 million

PER = 430/38,7 = 11,1 (but this does not include debt!)

EBITDA Adjusted Normalized = (63,2 - 2,4 + 2) x 12/9 = 83,7 million

EV/EBITDA = 683,5/83,7 = 8,2

Net Debt/EBITDA = 253,8/83,7 = 3

With respect to Free Cash Flow, I will exclude changes in working capital from the calculation, as some years benefit FCF and others are detrimental to it.

FCF (adj) = (CFO + changes in working capital - Capex) x 12/9 = (21,6 + 26,6 - 16,5) x 12/9 = 42,3 million

EV/FCF (adj) = 683,5/42,3 = 16

Market Cap/FCF (adj) = 430/42,3 = 10,2

Total current debt is $267 million. Normalized interest paid is 8 million (representing 3% interest). If they refinanced the entire debt at 7% interest, the interest on the debt would amount to 18.7 million. It is clear that rising rates affect TerraVest and its ability to borrow to make acquisitions. As debt payments rise, FCF could be affected.

Finally, for the record:

Dividend= 0,10 x 4 = 0,40 $CAD/share

Dividend Yield = 1,7%

If management manages to allocate capital as they have done in the past, I believe returns will continue to be good. For now I have no position in TerraVest but I will keep following it.

gran trabajo Oscar, super bien explicado, una empresa de picos y palas, muchas gracias por compartirlo, coincido, a estos precios no entraría, pero una pena no haberla conocido antes, y si tiene una buena corrección puede ser interesante, un saludo